How to Choose a PSP for High-Risk Industries in 2026 - TODA Pay

The payment processing landscape is crowded. More than 400 registered PSPs operate across Europe and North America alone — yet choosing the wrong partner can cost a merchant thousands of dollars in frozen funds, chargebacks, and compliance headaches. For high-risk niches — iGaming, crypto exchanges, subscription platforms — the stakes are even higher.

The wrong PSP doesn't just cost you fees. It can disrupt your revenue stream at critical moments.

Why Aggregated PSPs May Not Suit High-Risk Merchants

Stripe, PayPal, and most payment aggregators operate on a shared merchant account model — multiple clients pooled under a single acquiring relationship. For an iGaming operator or a forex trading platform, this structure can mean elevated exposure to account-level risk events that are outside any individual merchant's control.

High-risk businesses benefit from a dedicated merchant account, specialised underwriting, and a provider familiar with their specific niche.

7 Criteria for Selecting a High-Risk PSP

• Multi-jurisdictional licensing — Look for MSB registration, EMI licence (e.g. Polish EMI for EU access), and FINTRAC or FCA recognition. TODA Pay holds both MSB and EMI credentials, enabling compliant operations across Canada and EU-passported markets.

• Alternative Payment Methods (APM) support — Your customers want choice: e-wallets, Klarna, PaysafeCard, Trustly, open banking. A PSP limited to Visa/Mastercard may leave conversion opportunities unrealised.

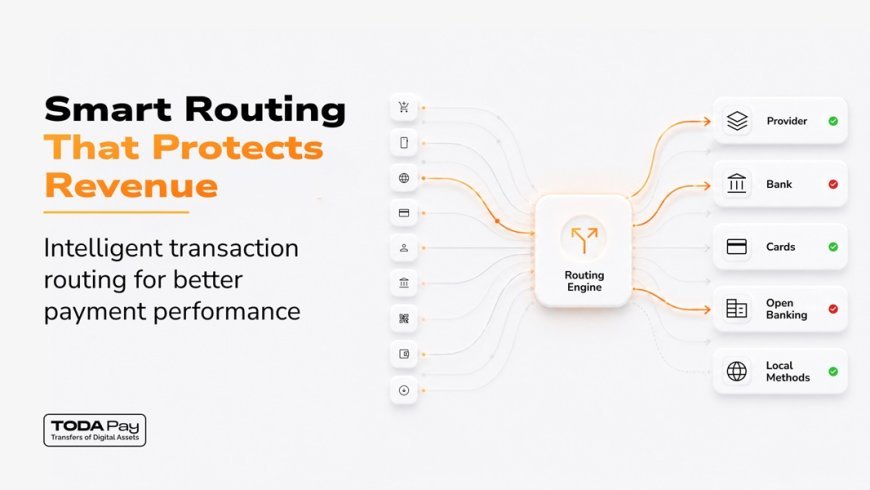

• Smart routing — Automatic transaction routing to the most approval-likely channel reduces the impact of individual acquirer outages on your acceptance rate.

• Flexible settlement options — SEPA, SWIFT, bulk payouts, and crypto settlement (USDT/USDC). Settlement speed and currency flexibility directly impact working capital management.

• Responsive support with defined SLAs — High-risk operators require reliable escalation paths. Verify the specific support hours and response time commitments in writing before signing.

• Transparent MDR with no hidden setup fees — A reputable PSP shows you the full cost structure upfront. TODA Pay operates on a fixed MDR model with zero setup fees.

• Fast technical integration — REST API, SDK, and no-code connectors. Target timeline from application to live MID is 2–7 business days, subject to completion of compliance review.

What Is Payment Orchestration and Why You Need It

Payment orchestration is an architecture in which a single provider manages multiple processing channels through one integration. If the primary channel declines a transaction, the system instantly reroutes it through a backup — a process called cascade routing.

According to available industry data, orchestration-based routing can improve acceptance rates by 15–30% for merchants with diverse transaction profiles. Individual results depend on merchant category, processing volume, and geographic mix. TODA Pay builds its infrastructure around this model, allowing merchants to access a global processor network through a single API endpoint.

Open Banking as a Competitive Advantage

Open Banking Payment — direct account-to-account transfers bypassing card networks — is one of the fastest-growing sectors in fintech. Processing fees typically run at 0.1–0.3% versus 1.5–3.5% for card processing, depending on the provider and transaction type. Chargeback exposure is substantially reduced relative to card-based processing, as A2A transfers are generally irreversible under PSD2-governed flows.

For iGaming operators, open banking deposits can reduce friction while lowering operational risk. TODA Pay's open banking solution covers EU markets via PSD2-compliant bank APIs, integrating with local banking apps.

What to Expect During Onboarding

A trustworthy PSP will request: a business plan or pitch deck, projected monthly volume, your MCC code, and full corporate documentation. Any provider promising 'instant approval without documents' warrants careful scrutiny. Expect a target timeline of 2–7 working days to live MID from the date all required documentation is received and compliance review is completed.

Final Thoughts

The right PSP is not just a technical gateway — it is a strategic partner. Invest time in proper due diligence: verify regulatory status, speak with support before signing, and request case studies from your specific niche. This is precisely the approach that distinguishes specialised payment providers focused on long-term B2B partnerships from generic processors chasing volume.

About TODA Pay: TODA Pay (todapay.com) is a Canada-based Payment Service Provider (SMART PAYMENTS TECHNOLOGIES LTD, MSB M20438511) offering Open Banking, APM, card acquiring, card payout, and crypto settlement for high-risk and high-volume merchants globally.

DISCLOSURE: This content is produced in partnership with TODA Pay. All regulatory claims have been verified against publicly available registration data.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0